The numbers behind South Africa’s migration patterns

Listen to the Kaya Biz interview here: Kaya Biz, 30 Jun Migration Reality Check: The Data Reshaping South African Business

South Africa is being reshaped by three simultaneous migration forces: a large inflow of regional labour, a structurally significant outflow of skilled citizens and massive interprovincial movement. Each carries direct implications for business, for talent pipelines, location strategy, consumer market development, and political risk.

In June, President Ramaphosa addressed the nation on migration and acknowledged failures in immigration management, while simultaneously condemning xenophobia, vigilantism, and attempts by private groups to police foreign nationals. Anti-immigration movement ‘March and March’ has set a deadline of 30 June for undocumented foreign nationals to leave South Africa, with a coalition of 27 civil society groups confirming plans for nationwide protests and threats to “shut down” the country if demands are not met.

“South Africa is being reshaped by multiple migration forces that all have an impact on business decisions,” says Eighty20. “Whether it be skilled professionals leaving, regional labour arriving, or millions moving toward economic opportunity at the urban edge. The businesses that read those signals correctly will find themselves where the markets and talent actually are.”

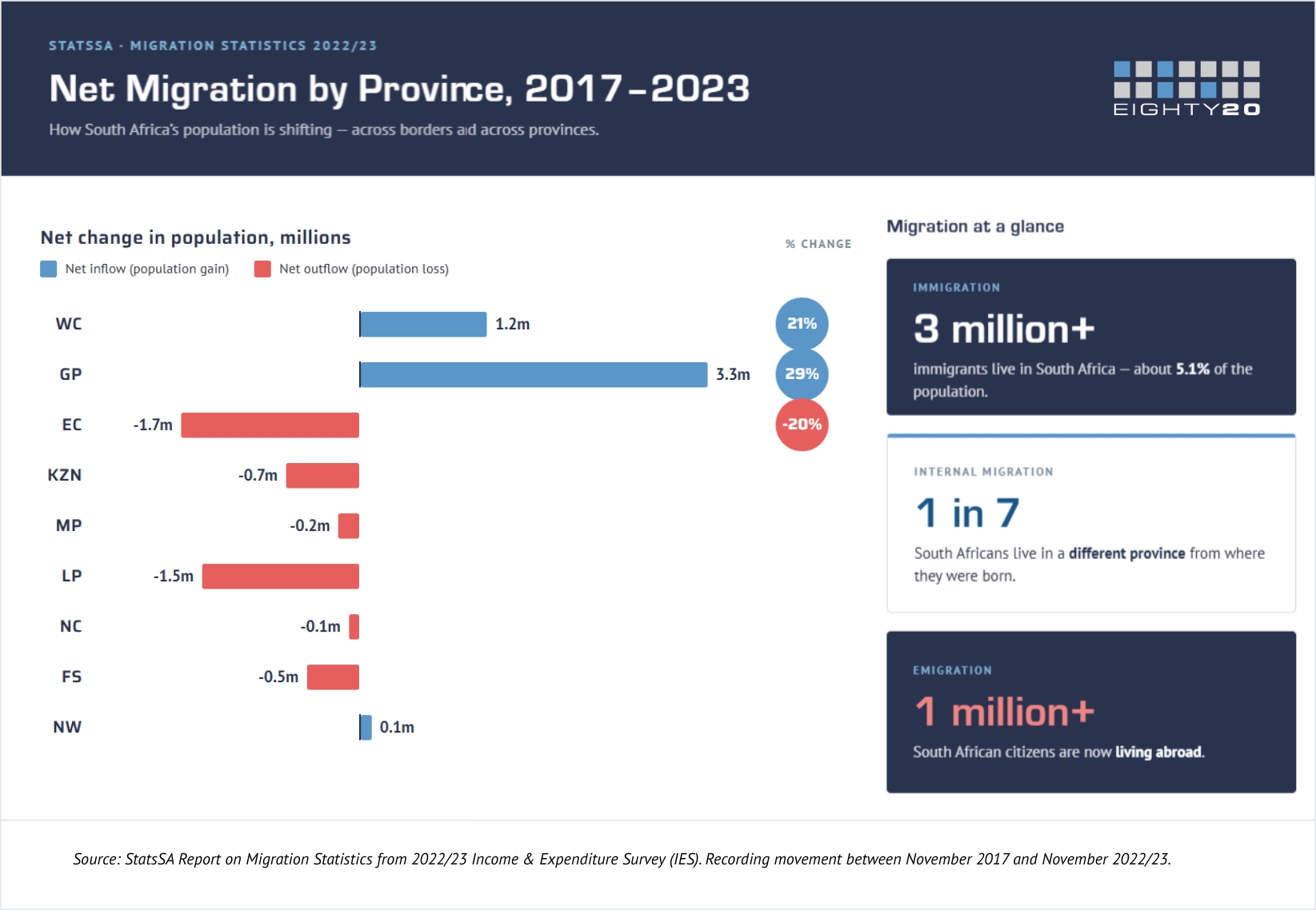

Migration data is among the most contested in South Africa. The undocumented population is by definition uncountable; foreign nationals have good reason to avoid formal surveys; and the Department of Home Affairs has not published immigration statistics since 2015. Emigration data is similarly weak, with Stats SA relying on modelled estimates rather than actual departure records. The result is a data vacuum that inflated claims and political rhetoric have been quick to fill. What follows draws on the most reputable available sources to give a clearer picture.

|

Arrivals in numbers

The 2022 Census recorded 2.4 million immigrants; the 2022/23 IES Survey, published in 2026 based on forecasted data, puts the figure at over 3 million, or 5.1% of the population. The true number is certainly higher. In a country where foreign nationals fear for their safety, Census enumeration systematically undercounts this population. The margin of that undercount remains unknown.

Nearly 64% of immigrants originate from SADC countries, with the top five sending countries including Zimbabwe (48.5% of the foreign-born population recorded in Census 2022), followed by Mozambique (20%), Lesotho (10.9%), Malawi (9.5%), and the United Kingdom (2.9%). The immigrant population is predominantly male, working age, and concentrated in Gauteng and the Western Cape.

Who is leaving and why this matters

The outward movement of South African citizens is smaller in volume but disproportionate in economic consequence. UN International Migrant Stock data updated to mid-2024 records just over one million South African citizens living abroad, up from 295 400 in 1990. Australia, the United Kingdom, the United States, New Zealand, and Germany account for the bulk of this population.

The concern is not the aggregate number but the composition. The top ~5% of taxpayers, which is a few hundred thousand people, contribute roughly a quarter of all personal income tax revenue. Losing even a few tens of thousands of high-earning professionals has measurable fiscal consequences, and a direct effect on the private sector talent pool.

|

The healthcare sector illustrates this most starkly: OECD data record more than 23 400 South African health professionals working in the UK, New Zealand, the United States, and Australia, with numerous public sector posts remaining unfilled for years as a direct consequence.

BrandMapp, a survey of South African households earning more than R10 000 per month, asks respondents to rate their likelihood of emigrating. Approximately 27% consider it likely or highly likely, a proportion that has not shifted since 2021.

Where the growth markets are forming

While the emigration and xenophobia narratives dominate headlines, another significant demographic shift is happening internally. Stats SA estimates that 9.1 million (one in seven) South Africans are lifetime migrants (a person currently living in a province different from the one in which they were born). The driver is consistent across every census period: the search for paid work.

Urban centres generate the vast majority of all economic activity nationally, and the population is following that concentration. Gauteng alone accounts for 38% of registered taxpayers and contributes 47% of the country’s personal income tax, despite representing only 25% of the total population. For the period 2021–2026, Gauteng is projected to absorb 1.4 million net new migrants, with the Western Cape absorbing nearly half a million.

Another data source that deals with the top end of the market, the Wise Move South African Migration Report draws data from nearly 6 000 interprovincial household moves. Relocations from the Western Cape to Gauteng increased nearly 60% year on year, but the Western Cape showed the strongest net inbound migration in 2025, with Cape Town being the strongest drawcard for its lifestyle benefits.

South Africa’s urban population grew from approximately 34.3 million in 2013 to 40.2 million in 2023 – an increase of 17% over the decade. The World Bank’s spatial analysis of South Africa’s urban footprint shows that the bulk of urban growth since 2000 has occurred not in city cores, but at their edges – in townships, backyard settlements, and peri-urban areas that function as the primary reception zones for internal and international migrants. Mass low-to-middle-income urbanisation is happening at the edges of Johannesburg, Cape Town, and their satellite towns.

What this means for business

Three strategic implications follow directly from the data. The first is talent – businesses are competing for skilled professionals who are more internationally attractive and mobile than ever before. Retention, international remuneration benchmarking, and graduate pipeline investment become key to success.

The second is market geography. Consumer growth is concentrated in peri-urban belts that most established businesses have been slow to serve. The businesses best positioned for the next decade are those orienting toward where South Africa is actually moving. Head of Marketing for one of South Africa’s fastest growing clothing retailers’ states: “The biggest retail growth opportunities lie in township and peri-urban markets, where proximity, value, and relevance matter most. It allows us to connect with more customers, support local economic ecosystems, and become a trusted part of the communities we serve.”

The third implication is operational and reputational risk. Xenophobic violence disrupts supply chains, damages employer brand, and deters the foreign investment and skilled talent that businesses depend on. Regardless of the number of migrants in South Africa, the political energy directed at this small minority is, at root, a proxy for frustrations about unemployment, housing scarcity, and service delivery failure, which are at their root structural failures with domestic origins.