The Golden Years on Credit: Financial behaviours of an aging population – deep dive into 2025 Q4 Credit Data

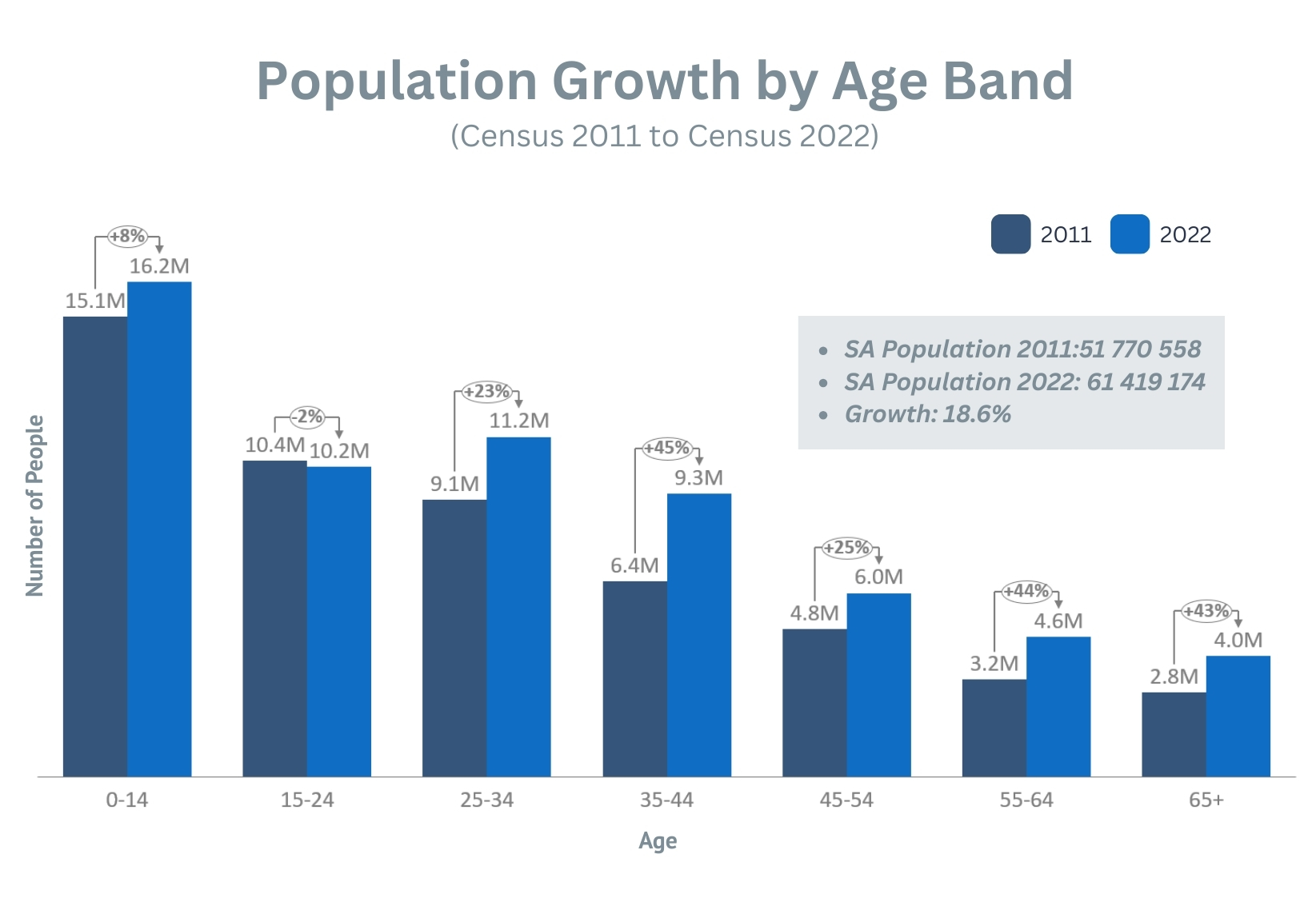

The number of South Africans in their ‘golden years’ is growing and accelerating. Census data shows adults aged 65+ increased from ~2.8m in 2011 to ~4m in 2022, a 43% rise against total population growth of just 19%. By 2070, the 60+ age group is projected to be the second most populous age category in the country.

There are numerous forces driving the rapid growth of the 65+ population worldwide. Medical advances, declining birth rates and improved living standards have extended life expectancy across the globe, while the massive post-war baby boom generation is now in its senior years. In South Africa, the expansion of anti-retroviral treatment has kept millions alive into old age. The United Nations projects that globally, the number of people aged 65 and older will double to over 1.6 billion by 2050, making the aging of the world’s population one of the most consequential demographic shifts in human history.

Seniors and Credit

Eighty20 releases a quarterly Credit Stress Report that examines consumer credit behaviour and the key economic events that impact South Africans (available here). The Eighty20 National Segmentation (ENS) is the lens through which it profiles South African consumer segments. The ENS has two senior segments, Humble Elders and Comfortable Retirees, who between them, took out roughly 840 000 new loans in Q4, (up 15% QoQ) but with dramatically different credit accounts.

Both segments face the financial difficulties associated with older people within the South African credit environment. These typically include low financial resilience, digital exclusion and the challenges and restrictions of living on fixed or limited incomes.

More so than the younger population, older adults often face rising living costs against fixed incomes, high medical expenses, dependant unemployed family members (reverse caregiving), and inadequate retirement savings.

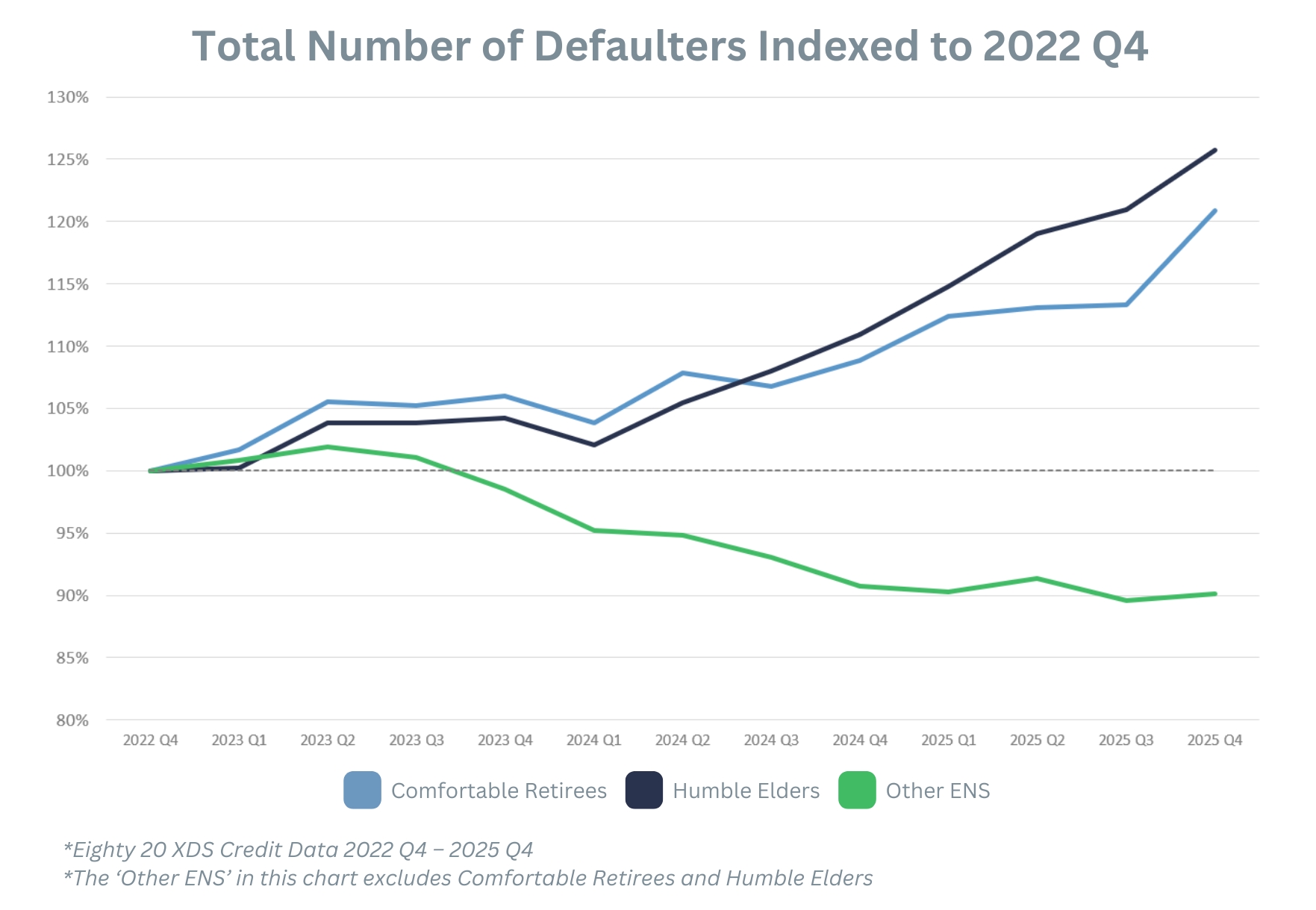

One worrying trend in senior credit health is the sustained rise in the number of defaulters, which appears to be accelerating rather than stabilising. A striking divergence has emerged between senior South Africans and the broader population: while defaulters across the general population have declined nearly every quarter since mid-2023, seniors have moved sharply in the opposite direction. Over the past six quarters, defaults among seniors have grown significantly, with Comfortable Retirees seeing a particularly sharp spike in the most recent quarter.

The Humble Elders

The four million South Africans who make up the Humble Elders segment are among the country’s most financially vulnerable – older, predominantly female, and struggling financially. This is the lost apartheid generation, who could not earn, save or invest throughout their lives so are now retiring dependent on family or state.

More than two thirds are single, and the vast majority depend on the SASSA Older Persons Grant, which provides R2 320 per month to the ~4m South Africans aged 60 and over who earn less than R9 000 monthly and hold assets below R1.5m. The average income in this segment hovers around R2 000 a month, a sum that barely covers basic survival, let alone unexpected expenses.

Humble Elders took out 610 000 new loans in Q4, heavily concentrated in retail accounts (70% of loans in 2025 Q4, up from 59% in 2021 Q4), with personal loans making up most of the remainder (27%). The average opening balance for this segment was R6 711 for retail loans and R4 385 for personal loans. Most don’t qualify for credit cards, so rely on these two credit products to pay household expenses and general living costs.

|

This segment increased their total number of loans by 16% YoY, with total loan balances growing by 13% in the same period. The biggest growth was in the number of personal loans (20%), and retail loans (14%). Further signs of stress saw the total number of defaulters grow by 13%, with overdue balances increasing significantly in overdue credit card debt (23%) and personal loans (10%).

The Comfortable Retirees

Comfortable Retirees are the second most affluent ENS segment. Made up of two million credit active and asset rich ex-professionals and middle- class consumers who benefitted from high earning jobs and retirement plans throughout their careers. Two thirds of them are retired, and are downsizing their lives, but the 300 000 who still have a mortgage make up 13% of all home loans.

Comfortable Retirees who took out 230 000 new loans in Q4 hold a more diverse portfolio than the Humble Elders, split evenly between retail accounts and credit cards (38% each), with personal loans (14%), home loans (6%), and vehicle asset finance (5%) rounding it out. The average opening balance for this segment was R10 523 for retail loans and R50 632 for personal loans. Their adoption of credit cards is second only to Heavy Hitters, averaging 1.5 cards per person.

While the segment grew by 10% year-on-year, their total number of loans grew at 18%, though total loan balances rose by a more modest 9.4%. The sharpest increases were in personal loans (19%) and retail loans (12%). Comfortable Retirees appear to have scaled back their secured credit exposure since last year, likely in response to the repayment pressures that such commitments entail.

|

The concentration in cards and personal loans points to a recurring theme: retirement income struggling to keep pace with consumption needs, and signs of stress are mounting. The total number of Comfortable Retiree defaulters grew by 11% year-on-year, while overdue balances climbed sharply across secured debt – VAF up 23%, home loans up 22% alongside a 22% year-on-year rise in overdue credit card debt. Taken together, this suggests many Comfortable Retirees are juggling payments and leaning on revolving credit to stay afloat.

This segment’s overdue balances have outpaced the broader credit market, climbing more than R7bn since 2022 Q4 to R22.3bn, and now representing 10% of total outstanding debt, compared to 8.4% for the broader market.

South Africa’s retirement crisis is already visible in the credit data. Rising defaults, swelling overdue balances, and growing reliance on unsecured credit reveal a population using debt to bridge the gap between retirement income and the cost of living – and struggling to keep up. Even the affluent Comfortable Retirees are showing accelerating signs of stress. The data tells a clear and sobering story: for too many older South Africans, the shine of the golden years is dulled by an increased dependence on debt.