Debt counselling can ease credit stress, but uptake remains low

Download the Credit Stress Report

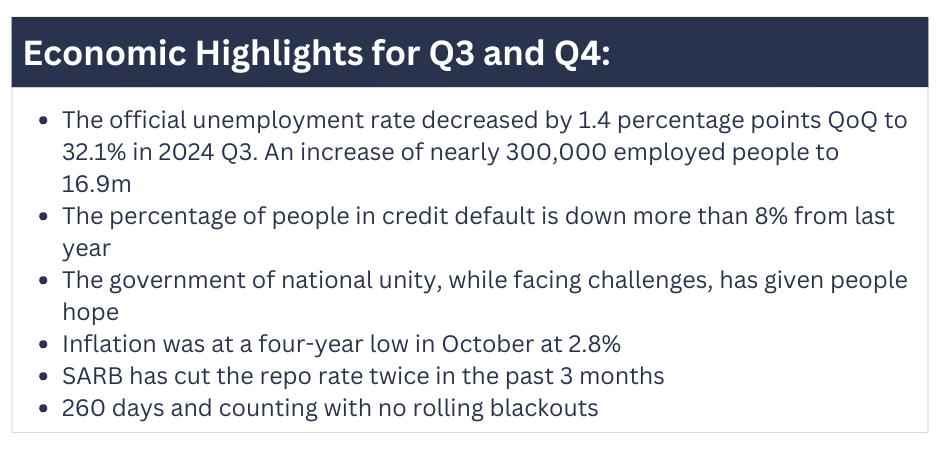

With the festive season upon us, economic indicators in South Africa are shining brighter than in many years, signalling renewed consumer confidence and potential growth in retail spending. Improved economic trends such as declining inflation rates, and improved employment numbers have contributed to a more optimistic environment for businesses and consumers alike. Additionally, there have been two repo rate cuts, personal default rates continue to drop, and 260 days and counting with no rolling blackouts. On top of that, the two-pot retirement system has put more than R35bn rand into people’s pockets.

One of the challenges of collating a quarterly report on credit and economic data is that it reflects past trends. While the positive developments in Q3 and Q4 of 2024 are significant, they likely had little impact on the Q3 credit data being reviewed, but will affect the future outlook. Unpacked below are key credit data indicators from Eighty20 and XDS.

Analysis: Q3 2024 Credit Data

The number of credit-active individuals continued to rise year-on-year, increasing by 1.4%, alongside a modest 1% growth in credit products. This quarter saw more than 900,000 new entrants to the credit market, signaling expanded access to credit.

Total loan balances are at R2.47trn, up by roughly R47.6bn (nearly 2% YoY), with a notable 40% of that growth coming from credit card and retail credit balances. Credit card balances, which were experiencing double digit growth for all of 2022 and 2023 have cooled to 6% YoY, but both total and average balances on credit cards are still outpacing inflation. On top of this, retail loan balances are up 5% YoY.

|

Total overdue balances are sitting at R194bn (8% of the total outstanding debt), which has grown by a modest R4.7bn in the year. Credit card and home loans are the only two loan products that showed significant growth in overdue loan balances YoY, with overdue balances on home loans up 23% and credit cards up 9%.

The continuing growth in credit card and retail loan balances, alongside the increase in overdue balances, suggests these products are being extensively utilized by consumers to cope with financial challenges, such as rising prices and stagnant salaries. The data underscores a growing dependence on high interest, unsecured credit products in a challenging economic environment.

On the positive side, the percentage of people in credit default is down more than 8% over the last year and has been dropping fairly consistently for 3 years. Notably, the proportion of loans in good standing (64.5%) was higher this quarter than in 2020 Q1 (62.0%), before Covid-19.

The latest data highlights a growing concentration of credit value among a smaller group of individuals. Total outstanding loan balances have experienced a compound annual growth rate (CAGR) of 5% since 2021, but only 1.4% CAGR in number of credit active individuals. Home loan balances are growing at a rate nearly 50X that of home loan holders since 2021. Credit card balances are growing at a rate that is 11X that of credit card holders.

Among the Eighty20 segments, the Middle Class and Heavy Hitters dominate credit markets, holding 93% of total home loan value and 80% of total credit card balances. “Despite their relative financial strength, these groups face alarmingly high instalment to net monthly income ratios, underscoring the precarious nature of their debt obligations. This trend highlights vulnerability even among wealthier segments, where high debt repayment burdens can quickly become unsustainable, leaving little room to absorb financial shocks,” adds Andrew Fulton, Director at Eighty20.

Debt Counselling

Many are unaware that debt counselling is an option if debt spirals out of control.

Debt review is a structured process in South Africa designed to assist individuals dealing with excessive debt. Through debt review, a debt counsellor will assess an individual’s debt and income and map out a feasible repayment plan. This plan consolidates all debt into one monthly payment, which goes through a regulated payment distribution agency (PDA). The PDA is responsible for disbursing repayments to each creditor. The debt review process aims to lower a person’s monthly financial obligations by extending the repayment term and negotiating reduced interest rates, helping them regain control over their finances. Typically, individuals complete the debt review process within 3 to 5 years.

|

Despite credit card balances rising more than 30% since 2021, and overdue balances reaching nearly R200bn, there is a shockingly low percentage of South Africans in debt counselling. While there has been a significant increase in application volumes over the last four years, there were only 177,000 applications last year. To put that in perspective, there are ~20m credit active people of which roughly 43% are in default on one or more loans. When a loan is in default, it means that it is more than three months in arrears. That means of South Africans in default, about 2% apply for debt counselling and of those that apply, nearly 90% are granted debt review, but only 22% see it through to the finish.

The average number of loans held by people who apply for debt review is around six credit facilities, which is the situation for about 10% of credit active South Africans. For the Eighty20 ENS segments, Mothers of the Nation – a low-income segment of predominantly domestic workers and cashiers average 1.62 loans, the Middle Class have on average 3.55 loans, and Heavy Hitters 4.86. Roughly 18% of the Middle Class and 34% of Heavy Hitters have more than 6 loans, and a concerning 6% of Heavy Hitters are paying instalments on 10 or more loans.

|

DebtBusters’ r Debt Index Q3 2024 finds that the average number of credit agreements per new customer is 7.1 in Q3 2024. Benay Sager, Executive Head at DebtBusters said “consumers need to spend 66% of their take home pay to service their debt, which is the highest recorded level since 2017”. Eighty20 calculations put the average Instalment to Net Monthly Income Ratio for all South Africans at roughly 30%, but for the wealthier Heavy Hitter segment it is closer to 50%.

While some economic indicators in South Africa are currently more positive than at any time in recent history, the period since the COVID-19 pandemic has seen many South Africans significantly increasing their credit holdings. This expansion of credit, combined with inflationary pressures and slower-than-expected wage growth, has created a precarious financial situation for many individuals. Debt levels have surged while disposable income has remained stagnant or even decreased for a large portion of the population.

In light of these challenges, debt counselling should become a consideration for consumers struggling to manage their financial obligations. This service can offer individuals a structured path to regain control over their debt, prevent defaults, and avoid more severe financial consequences.

Download the Credit Stress Report